[sg_popup id=”3″ event=”onload”][/sg_popup]

San Francisco Realtors learn to calculate debt to income ratios (DTI)

[vfb id=4]

WEBSITE: WWW.AGENTSANFRANCISCO.COM

415-796-0086 – HECTOR ALDANA

REALTOR! Can you income qualify a buyer.. Its Easy…

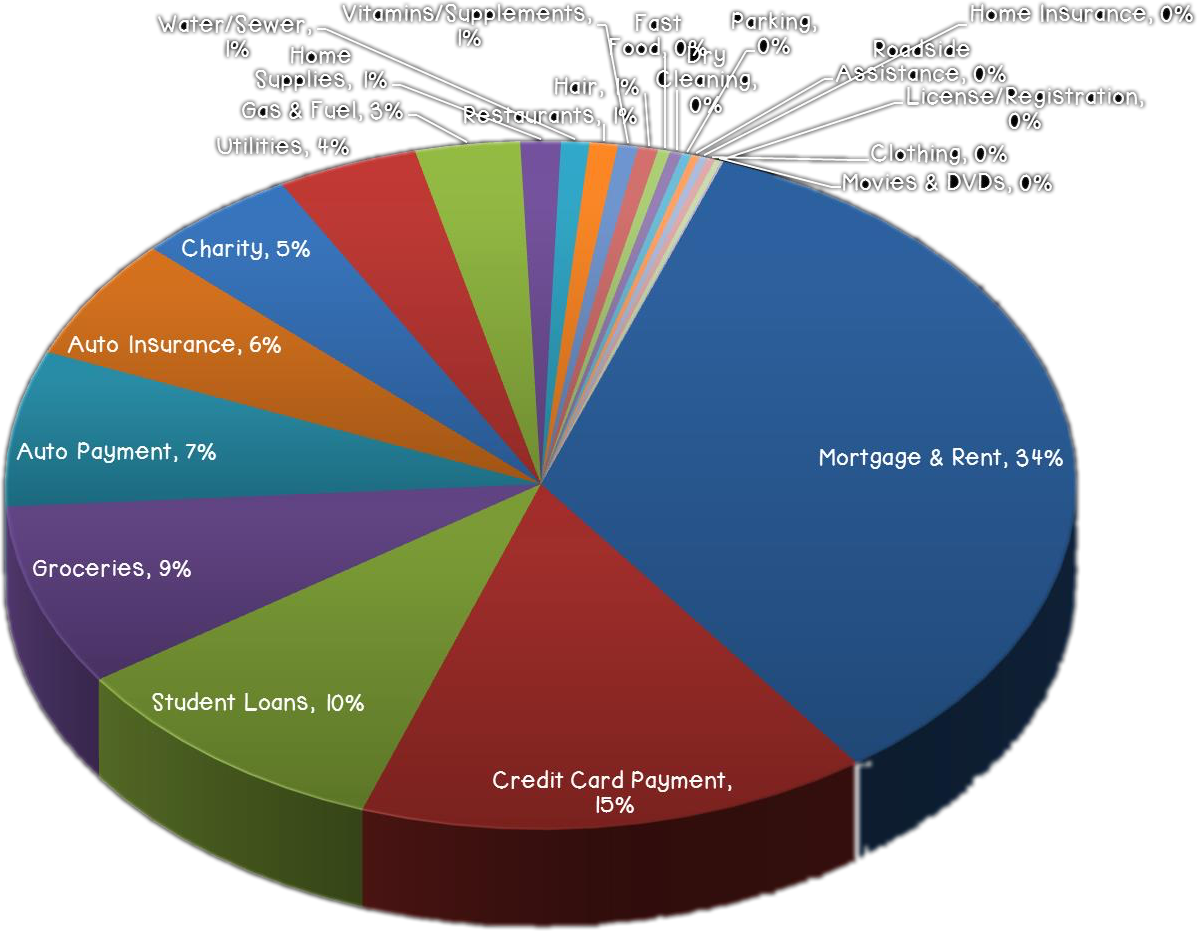

What is a debt-to-income ratio? Why is the 43% debt-to-income ratio important?

Answer: Your debt-to-income ratio is all your monthly debt payments divided by your gross monthly income. This number is one way lenders measure your ability to manage the payments you make every month to repay the money you have borrowed. To calculate your debt-to-income ratio, you add up all your monthly debt payments and divide them by your gross monthly income. Your gross monthly income is generally the amount of money you have earned before your taxes and other deductions are taken out. For example, if you pay $1500 a month for your mortgage and another $100 a month for an auto loan and $400 a month for the rest of your debts, your monthly debt payments are $2000. ($1500 + $100 + $400 = $2,000.) If your gross monthly income is $6000, then your debt-to-income ratio is 33 percent. ($2000 is 33% of $6000.) Evidence from studies of mortgage loans suggest that borrowers with a higher debt-to-income ratio are more likely to run into trouble making monthly payments. The 43 percent debt-to-income ratio is important because, in most cases, that is the highest ratio a borrower can have and still get a Qualified Mortgage. There are some exceptions. For instance, a small creditor must consider your debt-to-income ratio, but is allowed to offer a Qualified Mortgage with a debt-to-income ratio higher than 43 percent. In most cases your lender is a small creditor if it had under $2 billion in assets in the last year and it made no more than 500 mortgages in the previous year. Larger lenders may still make a mortgage loan if your debt-to-income ratio is more than 43 percent, even if this prevents it from being a Qualified Mortgage. But they will have to make a reasonable, good-faith effort, following the CFPB’s rules, to determine that you have the ability to repay the loan.

San Francisco Real Estate Agent with New listings and low interest rate loans